JPMorgan's £1.5 billion JPM UK Equity Core fund is not chasing the hoped-for recovery in smaller British companies, and it is keeping its money where performance has been strongest. As of March 31, 2026, more than 80% of the portfolio was in companies worth more than $10 billion, while just 1.4% sat in stocks below $1 billion.

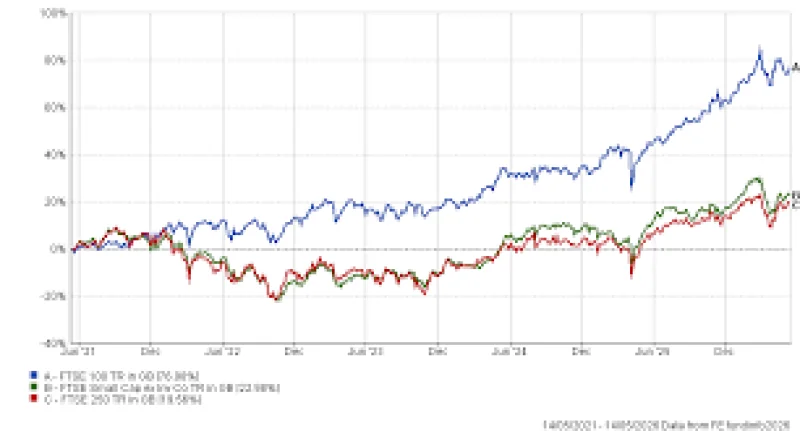

That stance matters because many UK investors have spent the past year waiting for the gap between large and smaller listed companies to narrow. But the fund, which sits in the IA UK All Companies sector, has built its asset base on a process that has repeatedly favoured large caps over fashionable rotation trades. Callum Abbot said that if investors were looking at the 2010s, they would have wanted to be overweight smaller and mid-cap companies, but that in the past five years the right call has been to focus on large caps. By the end of April 2026, the FTSE 100 had beaten both the FTSE 250 and the FTSE Small Cap ex Investment Companies index over one-, three- and five-year periods.

The numbers from 2025 underline why the debate has sharpened. The FTSE 100 returned 25.8% that year, compared with 13% for the FTSE 250 and 10.9% for the FTSE Small Cap ex Investment Companies index. That strength has helped support a broad view that large companies remain the cleaner trade, even as a separate article on the day's market moves showed Currys topping the Ftse 250 as UK hiring stalled and oil eased.

Abbot was not dismissing the possibility that smaller and mid-cap shares could recover. He said they look attractively valued on a cyclically adjusted basis, and he also noted that UK housebuilders trade at a discount to book value, while the sector normally trades at around 1.4 times book. But he argued that valuation on its own is not enough to justify a portfolio shift without a clear and credible catalyst to close the discount. In his words, he would never use the phrase never about any sector.

The tension in the market is that cheap does not always mean soon. Abbot pointed to banks as a reminder of how quickly an unloved sector can turn into a source of winners, noting that many managers once avoided them before some of the best-performing stocks in the FTSE emerged from the group since 2023. For now, though, JPM UK Equity Core is making the opposite bet from those waiting on a broad Ftse 250 rebound: it is staying anchored in large caps until the evidence for a smaller-company rerating is more than just a valuation argument.